This is the concluding post on the 4-part series, “Investing in Nigeria”. We have taken you on a journey exploring the meanings of each article and how these investment vehicles help turn a profit. Today, we talk about Bonds and extensively but simply cover what Bonds mean and how investors earn from them. Let’s dive in.

What are Bonds?

A bond is a fixed-income investment in form of a loan from the investor to a Corporation or Government.

In simple terms, it should be looked on as an I.O.U. Where the borrower (State, Government, large Corporation etc) uses the monies raised to finance Projects. The issuers are the borrowers while the investors are creditors or debt holders.

The details of a bond includes the include the end date when the principal (original investment) of the loan is due to be paid to the bond owner and usually includes the terms for interest rates.

How bonds work

Many corporate and government bonds are publicly traded; others are traded only over-the-counter or privately between the borrower and lender.

A face value of the bonds is determined and this is what is paid back to the investor. The actual market value of the bond is determined using a few factors like the borrowers reputation and credit quality, the general interest rate at the time of issuing the bond and the length of time the bond is to be held.

On certain dates, the issuer of the bond makes payments (interest) to the investor and at the point of maturity, the investor receives the face value of the bond.

It is important to note that government bonds are called by different names depending on the duration. Bonds with maturity less than 1 year are called bills (i.e. Treasury bills). Bonds between 1 – 10 years are called “notes” while those longer than 10 years are called “bonds”. The entire category of bonds issued by a government treasury is often collectively referred to as “treasuries”. It is also called Sovereign Debt.

Post Summary with Real World Example

This example Summarizes the Lesson on Bonds before we go into details.

If a company that needs to borrow $5 million to fund a new research, they could issue bonds because the bank would give them higher interests that they would pay investors, for example, 23%. They instead borrow from the public by issuing bonds with a 10% coupon that matures in 10 years.

Condition 1

If they knew that there were some investors willing to buy bonds with a 7% coupon that allowed them to convert the bond into stock if the result from their research increases the company’s stock price above a certain value, they might prefer to issue those bonds. This will be a Convertible Bond.

Condition 2

If the credit value of a company improves after 5 years or the government interest rate improves, they would be able to afford to give less coupon rates than originally expected because the demand for their bonds will skyrocket. So the company calls back or buys back the bonds to reissue at a lower coupon rate, this is called a Callable Bond

Condition 3

If the credit of the company starts to drop after 5 years, and investors decide to put back or sell back the bond before it reaches maturity, it is called a Puttable Bond

Characteristics of Bonds

Most bonds share some common basic characteristics including:

The issue price is the price at which the bond issuer originally sells the bonds.

Face value is the money amount the bond will be worth upon maturity. It is also called the par-value and is used in calculating interest rate.

The coupon rate is the rate of interest the bond issuer will pay on the face value of the bond, expressed as a percentage.

For example, a 5% coupon rate means that bondholders will receive 5% x $100,000 face value = $5,000 every year.

Coupon dates are the dates on which the bond issuer will make interest payments. This is usually semiannual payments.

The maturity date is the date on which the bond will mature and the bond issuer will pay the bondholder the face value of the bond.

Yield is principal plus the total interest paid is known as the yield, which is the total return on investment.

Resale – Most bonds can be sold by the initial bondholder to other investors after they have been issued. In other words, a bond investor does not have to hold the bond to the maturity date.

Repurchase – It is also common for bonds to be repurchased by the borrower if interest rates decline, or if the borrower’s credit has improved, and it can reissue new bonds at a lower cost.

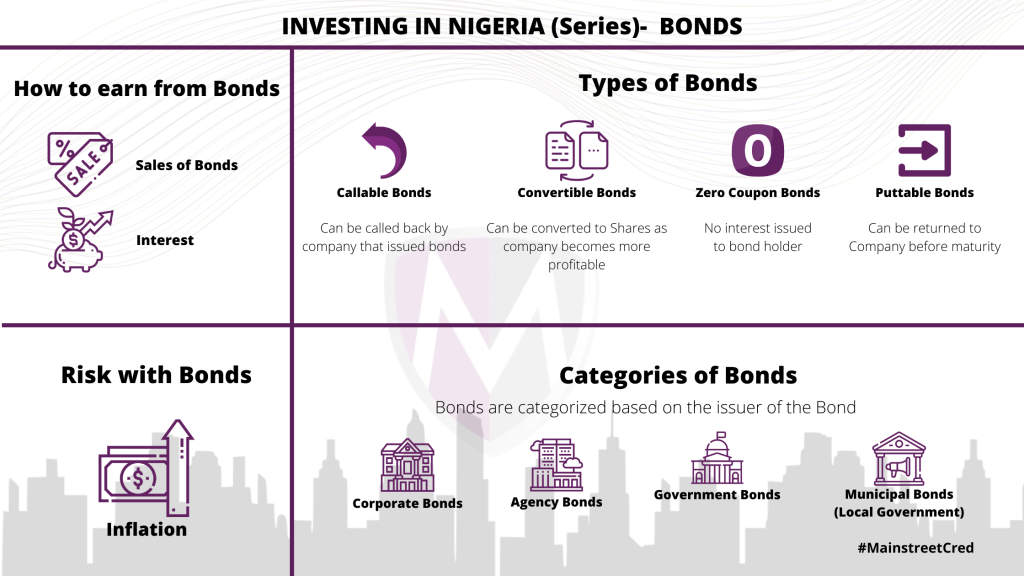

Categories of Bonds

Corporate bonds are issued by Companies. Companies issue bonds as opposed to bank loans bonds often give lower interest rates.

Municipal bonds are issued by states and municipalities (local governments). Some municipal bonds offer tax-free coupon income for investors.

Government bonds are issued by government. Usually sold to Financial institutions and sold to the market.

Agency bonds are those issued by government-affiliated organizations such as National Identity Management Commission or Federal Roads Maintenance Agency (Nigeria).

Infographic explaining bonds, categories of bonds, how to earn from bonds, types of bonds and the risks in bonds

Types of Bonds

It is usually a great idea to get asset manager to choose the kinds of bonds that one should invest in as there could be different combinations of convertibility rights coupon rates and other bond characteristics making each investment unique. Because there isn’t a strict standard for each of these rights and characteristics, getting a bond professional and Asset Managers that will meet their investment goals is key. Below are the 4 most common types.

Zero-Coupon Bonds These do not pay coupon payments and instead are issued at a discount to their face value so that they generate a return upon bond maturity. Simply put, the bonds sell at a less amount than the face value and then the investor receives the face value upon maturity.

Convertible Bonds These bonds give an option that allows bondholders to convert their debt into stock (equity) at some point, depending on certain conditions like the stock value. This is great for the company if they want to have low interest rate at the early stage of the investment. For the investor, they are taking more risk in that the value of the stock might not rise within the 10-year period but if it does, they are getting a lot more value by way of company shares.

Callable bonds A callable bond is one that can be “called” back by the company before it matures. A callable bond is riskier for the bond buyer because the bond is more likely to be called when it is rising in value. Because of this, callable bonds are not as valuable as bonds that aren’t callable with the same maturity, credit rating, and coupon rate.

Puttablebond This allows the bondholders to put or sell the bond back to the company before it has matured. This is valuable for investors who are worried that a bond may fall in value, or if they think interest rates will rise and they want to get their principal back before the bond falls in value. The bond issuer may include a put option in the bond that benefits the bondholders in return for a lower coupon rate or just to induce the bond sellers to make the initial loan. A puttable bond usually trades at a higher value than a bond without a put option but with the same credit rating, maturity, and coupon rate because it is more valuable to the bondholders.

How to Earn From Bonds

InterestThere are two ways of making money on bonds, the first of which is to simply collect the interest payments until the bond matures.

ResaleThe second way is to sell the bond for more than you paid for it, before the point of maturity. By selling the bond through a broker it’s possible to make a capital gain depending on what has happened to the credit quality of the issuer.

Risks in Bonds

Although generally considered “safe,” bonds do have some risk.

Credit RiskThis refers to the probability of not receiving your promised principal or interest at the contractually guaranteed time due to the issuer’s inability or unwillingness to distribute it to you.

Inflation RiskA high rate of inflation can affect your investment. Upon receiving your principal back if the prices for basic goods and services are far higher than anticipated, the value of the returns may have dropped.

Reinvestment RiskWhen you invest in a bond, regular returns are expected. If you have plans to reinvest returns and interest rates have dropped considerably, you’ll have to put your fresh interest income to work in bonds yielding lower returns than you had formerly enjoyed.

Liquidity RiskBonds can be far less liquid than most major blue-chip stocks. This means that once acquired, one might experience difficulty in selling bonds at top dollar. It is therefore advised that bonds are and added into investment portfolios with the intention to hold until maturity.

How to get Bonds

Here at Mainstreet Cap, we have a great team ready to talk to you about your options and the rates available to you, no matter the size of your investment portfolio. Reach out to us here or open an account with us here.

To Stay tuned for more updates; follow Mainstreet Capital Limited on social media ( LinkedIn | X | Instagram | Facebook ). Remember, the more you learn, the better equipped you’ll be to make sound investment decisions.For more information or personalized investment strategies that take advantage of the new economic realities, book a session with our expert asset managers.

![mainstreetCapitalLogo[White] - 02](https://mainstreetcapltd.com/storage/2025/11/mainstreetCapitalLogoWhite-02.svg)